👋 Welcome to A World Reconfigured - your guide to a world changed by climate, geopolitics and technology. I write about how climate change is creating a new world with new rules, and often cover topics like the ❄️Arctic, 🤷♂️Rare Earths and 💻Data Centers.

If you happened to receive this email from a friend, please consider subscribing. If you’re already a part of this community, I’d love it if you could recommend it to a friend.

TL;DR:

What’s this about:

Critical Minerals’ October 2025 watershed moment and its impact on innovation

Project Vault as a potential market-making move for startups

Who knows, maybe your linkedin feed will soon be flooded by entrepreneurs going into mining innovation

Big Week for Critical Minerals

Last week was a big week for Critical Minerals at the best party in town, the 2026 Critical Minerals Ministerial:

Naturally, the Ministerial generated plenty of headlines and there was no shortage of announcements and deals: FORGE, Vault and a host of bilateral deals took center stage as US leaders took to the podium.

Equally naturally, there were plenty of takes by the broader community. Some of my favorites include:

✍️ Mike Froman gave the broader geopolitical context of the Administration’s moves

✍️ Amanda van Dyke provided historical context of stockpiles and provided a helpful analytical framework to think about Vault

🖇️ Ashley Zumwalt-Forbes talked about the different aspects of Vault and its comparison to the Strategic Petroleum Reserve

🌐 Dr. Gracelin Baskaran released an overview of Vault

Vault, the $12B critical mineral stockpile that was announced created waves and was at center of attention, with good reason.

I also became somewhat obsessed with it, but for a different reason than most takes out there. I think it is a prime example of how geopolitics reshape tech and venture.

Before we get into Vault and what it means for startups, let’s take a look at innovation for critical minerals.

Throwing Innovation Out There

We’re still in the early days of the Western response to China’s dominance over critical minerals. In this multidimensional game of mineral chess, not all pieces were moved.

FORGE, Vault and other tools are just the opening plays. So far, Vault seems promising, though there are many open questions.

One thing is patently clear: The US and its allies are increasingly willing to make market-moving plays and are willing to invest to catalyze the private market into action. Some scholars argue that Vault is a move that is trying to out-China China, but I don’t think so. I think this is move plays exactly to the strength of a superpower that shaped a world order based on private power.

Governments made their move (at least for now). The question is: Are venture investors listening?

Innovation as a Critical Lever

Innovation in a critical piece of the puzzle. New technologies have the power to reshape geopolitics (Internet, Social Media and AI are prime examples). In the mineral context, there are some interesting examples of innovation:

AI-enabled exploration and mapping

AI-enabled separation method discovery (like AI Drug Discovery but for mining)

Advanced Drilling and Mining Capabilities

Advanced recycling and reprocessing methods

Mine operation digitization (robotics, autonomous drilling)

REE alternatives

Just like with regulation, the term innovation is often thrown out there without discussing where it will come from, what the roadblocks are and how can we lift them.

There are many sources of innovation, from startups to corporate R&D. The problem is: time. Or, more likely, lack of it.

That is why venture-backed startups are probably the most important type of innovation, with their ability to move and break things.

Venture-back startups require venture capital, and investors are often not too keen on investing in complex, traditional, capex heavy industries, ones that are prone to geopolitical and operational risks.

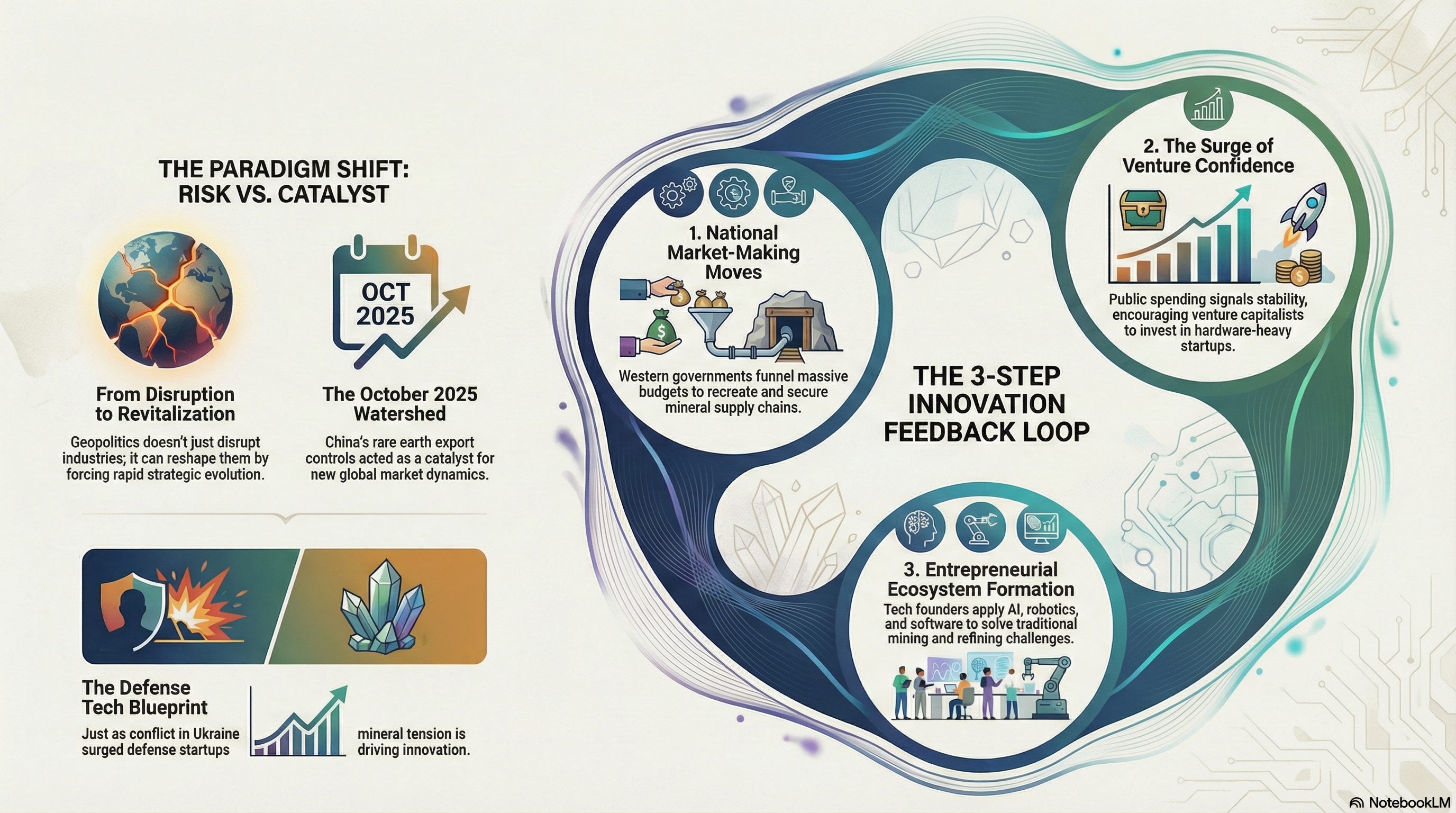

Geopolitics is Not Only a Risk

There’s a tendency to look at geopolitics as a risk factor. We often ask if an industry is prone to geopolitical disruptions (be them economic, military or social). But Geopolitics is not only a risk, but can also revitalize or reshape an industry. For example, geopolitical realignment, heightened great power competition and resurgence of conflicts (primarily in Ukraine) led to a surge in defense expenditures, which led to a wave of investments in new defense startups1.

By the same token, I believe that the Export Controls levied by China in October 2025 on rare earths was a watershed moment that is sending ripples through time, while catalyzing new market dynamics.

I believe this watershed moment will be met by a world eaten by software, AI agents and robots. They will eat critical minerals with the same enthusiasm with which they devour any other industry. To be clear, software will not eat minerals, but the supply chains they rely on, from mining operations to refining. There are already companies leveraging AI for exploration.

Yes, critical minerals innovation is engulfed by difficulties, roadblocks and market failures. There are reasons why traditionally there was scant interest in innovation in minerals. Tech was mostly not interested.

But, the shockwaves of October 2025 will change that, thanks to the renewed focus and global interest in the geopolitical moment we’re in, one where China is the defacto mineral czar of the world.

The logic is pretty simple:

The renewed interested yields, and will continue to yield, market-making moves by the US and the West, which will mean national-scale budgets funneled to recreating mineral supply chains.

Meaningful capital flows, increased demand for minerals and enhanced demand for better ways of doing things will create a market opportunity at a scale meaningful to attract venture investors, looking to enter new industries.

Venture investors will start signaling to innovators that there is a meaningful opportunity. They will do so with conferences, events, annual letters, incubation programs and, well, podcasts.

Entrepreneurs will take the hint and will move to apply general-purpose technologies and specialized innovations to critical minerals

A feedback loop will be created, and the ecosystem will form

We’ve seen this happen before: ClimateTech venture funding surged after the IRA signaled hundreds of billions in sustained policy support. DefenseTech saw the same pattern when Ukraine demonstrated the ROI of autonomous systems and Washington opened the checkbook.

Massive government spending creates conviction that the market is real, which gives VCs permission to deploy capital into categories they previously ignored.

Granted, Critical Minerals are not Defense. But they are similar enough for us to pay attention.

Both face long development cycles, have national security framing that justifies non-market pricing, and concentrated customer bases where government demand can overcome early-stage financing gaps.

Defense startups’ product market fit received a boost from Pentagon purchasing. Critical mineral startups face the same dynamic: if Vault and similar initiatives signal sustained government procurement, the risk calculus shifts quickly.

Arrival of Tech

Tech hasn’t “arrived” yet for critical minerals.

You can feel the vibe shift when tech "arrives". You can't miss it: Conferences, podcasts, meetups, linkedin posts. You know when tech arrives when you almost wish it didn't.

That didn’t happen yet, but I have a feeling that at some point we will start seeing things like this:

Jumping into the Vault

To get a sense of what kind of market-making initiatives are coming for Critical Minerals and what they might mean for startups, Vault is an instructive example.

Vault, like the name suggests, is a stockpile of critical minerals that was announced by the Trump Administration:

Vault is a stockpile. Like its name suggests, it is meant to buy minerals deemed by the US as critical2 for a rainy day. Judging by the happenings of October 2025, that rainy day just might show up sooner rather than later.

How does Vault work? Well, Vault isn’t an actual vault. It would be funny if it was, thought. At any rate, it is a $12B public-private partnership that is intended to buy and store minerals and provide access on pre-agreed prices.

The brunt of the financing comes from the US Export-Import Bank (~$10B), with the rest ponied up by corporate backers like GE Vernova and Boeing, as well as private investors. Participants can draw minerals when a major disruption occurs at a pre-agreed price.

Yes, it’s kind of like a Strategic Petroleum Reserve, but for minerals. Yes, I wish it looked something like this:

Why Do We Need Vault? Well, because of China. This reserve is supposed to curb China’s dominance by allowing participants with a buffer in face of exogenic shocks. What those shocks could be? Aside from plagues, export controls come to mind.

Vault, at least in theory, will allow participating companies (all from Allied countries) to gain access if China decides to pull the plug.

Is Vault perfect? I mean, who/what is?

$12B won't rebuild entire supply chains that China spent decades dominating. But that misses the point. Vault isn't trying to replace Chinese capacity overnight; it's creating proof that Western buyers will pay for non-Chinese supply at scale. As explained by a recent CSIS analysis:

Participating manufacturers do not receive access for free. Instead, they make long-term commitments to the program and pay a commitment fee in exchange for access to specified materials during market disruptions.

That credible demand signal is what unlocks private capital. Think of it as a down payment that makes the rest of the fundraising possible, not the full purchase price.

There are even more uncertainties and many open questions (here are a few of the important ones). In general, stockpiles are a great tool to buffer from disruption, but will not likely reduce dependency on China, which currently refines upwards of 90% of critical minerals and rare earths.

Vault’s consequence for startups and innovation is monumental.

What does Vault mean for Startups?

Startups fuse together entrepreneurial fervor and intensity, new technological solutions to old problems and lots of cash. To grow, they need plenty of things, but it boils down to clients and money.

As we’ve explored above, the key issue is that majority of venture investors have an aversion to risky, uncertain markets that are exposed to geopolitical risks at the magnitude of, well, China. China’s dominance, along with how would-be customers behave means that critical minerals, from mining to refining to integration, is mostly considered not worth the risk.

Institutional investors often have the opposite problem: They won’t shoulder the tech risk that is the bread and butter of startups.

Vault has the potential to change this.

In short, Vault provides startups with:

Offtakes and price stability

Streamlined go-to-market channels

Market Signal (“this is real”)

Pickaxes and Shovel Opportunities

We’ll take a look at each one separately, but also recognize the uncertainties.

Offtakes

What’s this: Offtake agreements are where a stockpile like Vault becomes a lifeline rather than a headline. If a startup knows it can sell a defined slice of future output at an agreed price into a government‑backed buyer, it suddenly has something concrete to show a bank or a fund instead of a pretty slide about “total addressable market.”

It doesn’t mean the startup gets to walk away scot-free, but investors usually look at offtakes as bankable revenue that can anchor project finance and bridge the terrifying gap between FOAK and scale.

Streamlined go-to-market channels

Most young companies in mining, refining, or materials learn the hard way that their problem is not just chemistry or geology, it is go‑to‑market. Industrial buyers are fragmented, conservative, and slow, each with its own specs and legal boilerplate, so sales cycles are measured in years, not quarters.

By aggregating demand from large players and standardizing some of the terms, Vault can act as a pre‑configured channel: if you qualify once, you effectively plug into a pool of customers instead of courting each one from scratch.

Market Signal (“this is real”)

For investors, the existence of Vault is as much a political signal as it is a procurement mechanism. When the U.S. government lines up $12B, export‑credit backing, and marquee corporates around critical minerals, it tells LPs and strategics this is not a passing fad that dies with the next headline cycle.

That does not guarantee any given startup a ticket, but it lowers the “policy rug‑pull” risk that has haunted the space and makes it easier for funds to underwrite multi‑cycle theses in mining, refining, and upstream materials.

In ClimateTech, the Inflation Reduction Act helped accelerate the development and commercialization of batteries, green steel and even solar and wind and brought much energy into venture investments.

Pickaxes and Shovels Opportunities

Finally, a stockpile on this scale creates an entire layer of “pickaxes and shovels” where founders never have to touch ore themselves. Someone has to build the logistics software, inventory management, quality tracking, cybersecurity, and recycling systems that keep a distributed reserve of sensitive materials secure and efficient.

These innovations tend to show up after major crises take place or in the wake of major technology disruptions. We’ve seen this playout with Cybersecurity, which has expanded from “pure play” into particular industries: First it was OT security; then, it was healthcare, and now we are starting to see verticalized cyber solutions for utilities.

What makes this different from selling software to existing mining companies? Scale and coordination. A distributed stockpile across allied nations requires cross-border tracking, real-time quality assurance between dozens of facilities, and provenance verification that no single mining operation has ever needed. That complexity creates greenfield opportunities where incumbents don't have entrenched solutions and startups can set the standard.

Taking Stock(pile)

Vault provides 4 distinct advantages to startups, Granted, there are uncertainties with each one: Offtakes still need to be better defined; market signals takes time; venture might be slow to respond; and not all verticalized offerings find a real market. We’ll have to see how they develop over time.

However, the bigger picture is more important, especially since Vault is not the end-all-be-all move. We can expect more market-making moves and initiatives that will be announced in coming months and years. Each one of the moves doesn’t have to be perfect, but rather help catalyze the market.

The US is not alone in this. We can expect Europe, Canada, Japan and other countries to announce their own initiatives, stockpiles or otherwise. They might appear in country-by-country form or in a Middle Powers amalgamation.

They can come in the form of more stockpiles, Buyers’ Clubs, Government Incentives or even regulatory requirements. Like with DefenseTech or ClimateTech, it is likely that the massive shifts that are taking place “thanks” to October 2025, the AI-ification of everything and geopolitical realignment more broadly will lead to more venture investments.

We should hope so.

I’m already looking for the Linkedin posts.

Thanks for reading! If you enjoyed this edition, don’t forget to subscribe or share your thoughts. 🔽

See you next week!

I will concede it is more complex than that. There’s the issue of AI and softwarization of war, and more. However, it is patently clear that geopolitical realignment had much to do with it.